Asia & MENA video game revenue to surpass $100 billion milestone by 2030

Evergreen games and direct-to-consumer monetization to drive multi-dimensional growth.

Note to Reader: This post offers a partial set of key takeaways from Niko’s 2026 Market Model Reports. Please fill out this form to automatically receive a free PDF of the complete set of takeaways at the regional and sub-regional level.

Player spending on video games in Asia & MENA increased at a faster pace in 2025 compared to the prior year, and the market continues to demonstrate resilience and long-term growth potential amid ongoing geopolitical uncertainty, shifting trade policies, and broader economic volatility impacting industries worldwide. Many markets in the two regions surpassed revenue expectations published in 2025, and consumer spending patterns, an expanding player base, and multi-dimensional growth are key factors at play.

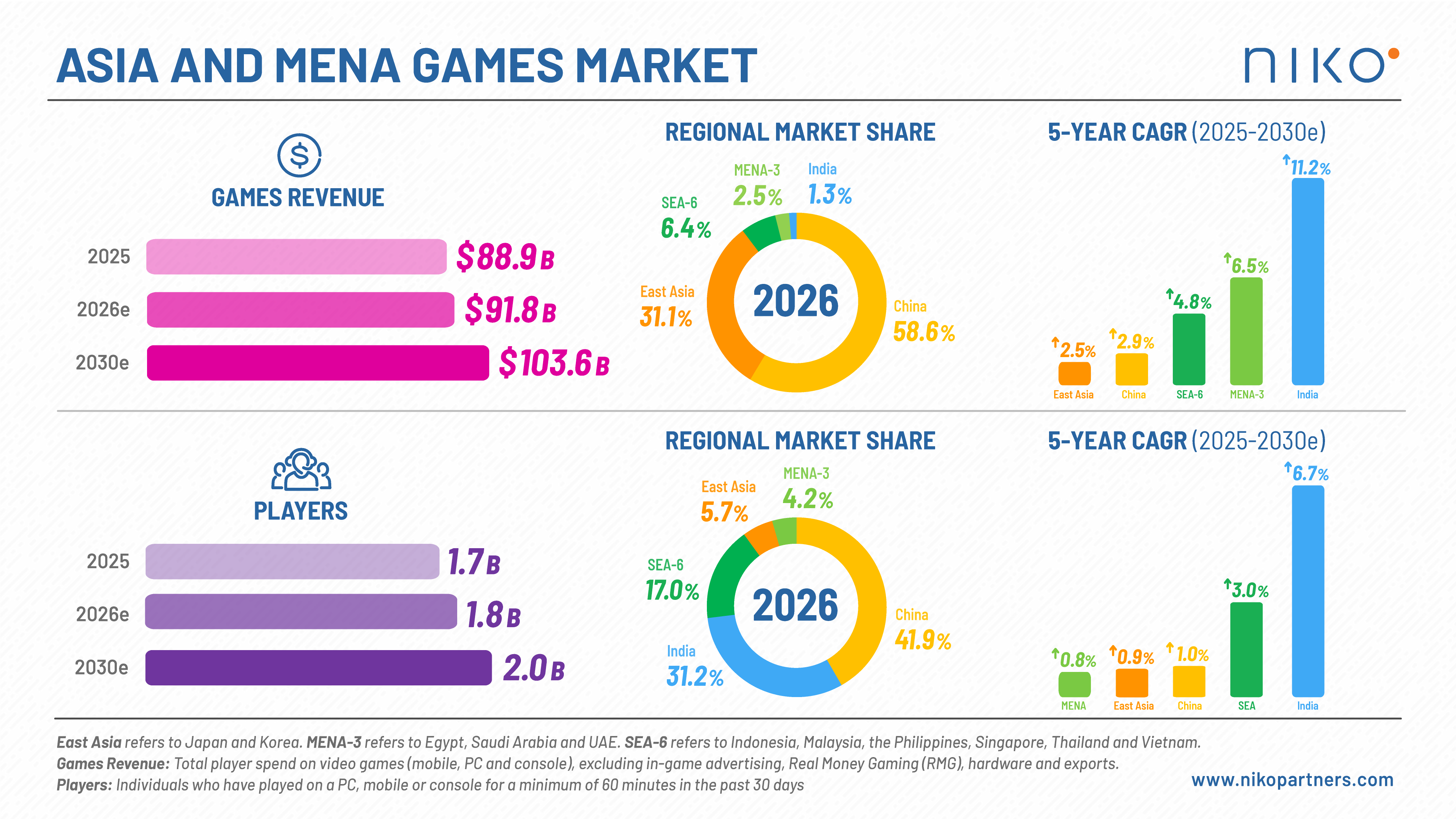

The Asia and MENA video games market generated revenue of $88.9 billion in 2025, up 2.6% YoY. Looking forward, growth looks even stronger, with the market projected to climb 3.4% in 2026 to $91.8 billion, and reach $103.6 billion in 2030, at a 5-year CAGR of 3.1%. The 13 markets that Niko Partners tracks account for approximately 46.3% of global video game revenue (our model excludes console gaming in Southeast Asia where it is not as prevalent). Total number of players will rise 3.5% in 2026 to 1.77 billion and reach 1.99 billion in 2030 at a 5-year CAGR of 3.1%.

While China, Japan and Korea are the most mature markets in Asia & MENA and will account for an impressive $91.7 billion in player spending in 2030, representing 88.6% of total revenue across the 13 countries we track, the most exciting growth stories remain elsewhere.

India has surpassed 500 million players and is set to become a nearly $2 billion market by 2030, with player spending growing at a 5-year CAGR of 11.2%. It is the fastest growing market we track.

Despite geopolitical instability, MENA-3 (KSA, UAE, EGY) is set to remain the second fastest growing region by revenue behind India, with player spending set to reach $3 billion in 2030. Annual ARPU in MENA-3 is set to increase by $10 over the next 5 years.

Thailand, the Philippines and Indonesia will be the fastest growing markets in Southeast Asia, with Thailand on track to reach the $2 billion player spending milestone next year and Indonesia to reach $1.5 billion by 2030.

Alongside India, Indonesia and Vietnam will see the fastest growth in players over our forecast period, with 144 million and 68 million players by 2030, respectively.

Game companies can now pursue a two-pronged strategy when it comes to Asia & MENA, targeting high ARPU segments in mature markets like China and East Asia while scaling up in emerging markets of India, Southeast Asia and MENA to reach a new demographic. Here are 5 key trends driving growth across Asia & MENA today:

The players split by gender will see females continue to rise, expanding the addressable player and payer base across Asia & MENA. Women now account for 42% of players in the region, up from 39.5% last year and surpassing the 40% threshold for the first time. Growth has been particularly notable in markets such as India and the MENA-3 which skewed 80% male 5 years ago and earlier, highlighting how gaming is becoming increasingly mainstream across gender.

Nintendo Switch 2 is driving console growth following official launches in Southeast Asia and MENA last year, alongside stronger-than-expected performance in Japan and China. Asia & MENA sales for Switch 2 are nearly 70% higher than the original Switch when launch aligned. Looking ahead, 2026 will be a stellar year thanks to the launch of Grand Theft Auto VI. However, we caution that increased pricing for console hardware may limit true mainstream adoption across the region.

Direct-to-consumer monetization is emerging as a major structural shift across Asia & MENA’s gaming ecosystem. Regulatory changes have enabled publishers to expand out-of-app monetization strategies, with more than 30% of players in Asia & MENA now preferring to transact outside of the game application itself. Over the next five years, we see publishers building deeper relationships with players as they bypass traditional walled gardens.

Growth across Asia & MENA is increasingly multi-dimensional – taking place in several gaming segments. Japan’s PC gaming market is continuing to surge and is expected to grow 8% this year. In China, mini games have become a significant growth segment, now accounting for nearly 20% of mobile game spending. In India, player spending on mobile games will surpass $1 billion in 2027, driven increasingly by spending outside the battle royale genre that has historically dominated the market but has since lost share to other genres.

Generative AI use in the video game industry has emerged as a polarizing topic globally, although player sentiment in Asia remains materially more positive than in Western markets. The majority of Asia based studios are already using AI tech and studios are increasingly reporting development efficiencies. However, player acceptance remains nuanced, with players generally more supportive of GenAI being used to assist development workflows rather than replacing core art assets or marketing content.

Publishers must move beyond a one-size-fits-all strategy and build market specific approaches that resonate with players. Other notable trends to watch include a shift to more transparent and player friendly monetization, increased consolidation around evergreen games (which Niko has published a recent whitepaper covering), a further rise in UGC tools, platforms and monetized experiences, and evolving youth digital restrictions impacting game platforms.

We also caution that currency fluctuations, rising memory prices, inflationary pressures, and geopolitical instability, including the 2026 Iran conflict, are exerting pressure on discretionary spending across gaming hardware, software, and services. While these factors are likely to slow hardware upgrade cycles and constrain spending growth among some consumers, Asia & MENA are still expected to outperform global market growth through 2030 as a larger secondary cohort of paying gamers begins to emerge across the regions.

Download the key takeaways by region via this form. Contact research@nikopartners.com for any questions about our research and service or learn more about our Market Report Series covering 13 markets: China, India, East Asia (Japan, Korea), SEA (Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam), and MENA-3 (Egypt, Saudi Arabia, UAE).